Consumer and commercial banking products and services are offered through CIBC Bank USA. Member FDIC and Equal Housing Lender. All loans are subject to credit approval. Trust services and investment products are offered by CIBC Private Wealth Management. CIBC Private Wealth Management includes CIBC National Trust Company, CIBC Delaware Trust Company and CIBC Private Wealth Advisors, Inc. (a registered investment adviser) all of which are wholly owned subsidiaries of CIBC Private Wealth Group, LLC — and the private banking division of CIBC Bank USA. Trust services and investment products are not FDIC insured, not deposits or obligations of, or guaranteed by, CIBC Bank USA or CIBC National Trust Company, and are subject to investment risk, including loss of principal.

Commercial real estate products and services offered by CIBC Bank USA and CIBC Inc.

CIBC Capital Markets is a trademark brand name under which CIBC and some of its subsidiaries, including CIBC World Markets Inc., CIBC World Markets Corp. and CIBC Bank USA, provide different products and services. Capital Markets products are not FDIC insured; not deposits or obligations of, or guaranteed by, CIBC Bank USA; and are subject to investment risk, including loss of principal.

This website is not intended for use by residents of the European Union (EU).

The CIBC Logo is a registered trademark of CIBC, used under license.

©2026 CIBC Bank USA.

We provide the latest developments and potential economic impacts and implications of the evolving tariff situation

Latest developments

This weekend, President Donald Trump announced plans to impose a 25% tariff on most imports from Canada and Mexico and an additional 10% tariff on Chinese goods. These proposed tariffs cover over $1.2 trillion of traded goods1 and are reported to be the largest protectionist act by the US in over a century. Negotiations played out in real time on Monday when both Mexico and Canada negotiated 30-day delays in the start date in exchange for measures to tighten border security. Tariffs on China went into effect as scheduled and have been called an “opening salvo” by President Trump.

Tariffs were a well-known tool of the Trump 1.0 administration and a prominent feature of the Trump 2.0 election campaign. Despite this, markets opened with a negative tone on Monday, with US equity futures down as much as 2% overnight. Equity, bond and currency levels have been factoring in a high likelihood of restrictive trade policy for months, but there were several elements of uncertainty facing markets prior to this announcement.

Many believed President Trump was using the threat of tariffs as a negotiating tactic, or that the actual amounts would be muted by carve outs, exceptions and legal challenges. Instead, the tariffs announced over the weekend were wide reaching with the only exception being a lower rate for Canadian oil. Following yesterday’s negotiated pause, there could be adjustments to the amounts in either direction, pending ongoing discussions. All three trading partners have announced or planned retaliatory measures, and Trump stated an intention to raise penalties further in response.

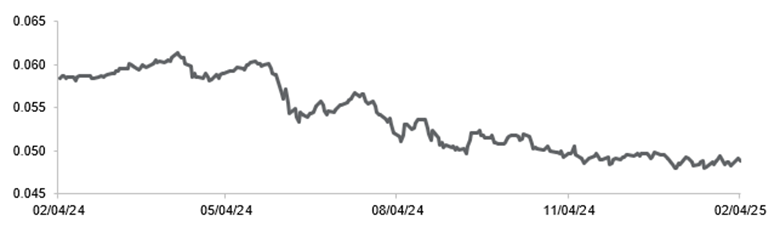

Domestically, markets have seen ups and downs as investors attempted to balance the positives of deregulatory orders and the potential extension of income tax cuts against the disruption of restrictive trade policy. Market sentiment may be clearer if you look at currency action. As seen in Exhibit 1, the Mexican peso depreciated against the US dollar by over 25% since March of 2024. The weight of a 25% tariff on Mexico’s competitiveness may have already been muted by movement in the exchange rate.

Exhibit 1: Price of one Mexican peso in US dollars

Source: FactSet as of February 4, 2025.

Economic impact and implications

The US economy is in a relatively strong position and should be able to weather short-term disruptions. Fourth quarter US gross domestic product (GDP) grew by an annualized rate of 2.3% with consumption growing by over 4%. Additionally, consumption of services represent almost twice the amount of traded goods in the US.

The Federal Reserve (Fed) will be watching for the impact on growth and inflation as a result of the new policies. Recently, the Fed’s easing campaign was paused, in part, to assess the impact of any tariffs on the economic outlook. Should trade disruption weaken the economic outlook, the Fed could restart a rate cutting strategy. This will depend on the degrees to which tariffs are passed through to consumer goods prices and longer-term inflation expectations rise. If markets look through the near-term tariff increases as temporary hits to goods prices, the Fed will have greater latitude in lowering interest rates.

We will be watching for further negotiations. The book is not closed on this chapter of trade policy, and Trump has already hinted at plans for protective measures against Europe, among others.

We will continue to monitor and keep investors apprised of the evolving tariff situation. If you have any questions, please do not hesitate to contact a member of your Private Wealth team.

Gary Pzegeo, CFA,is co-chief investment officer of CIBC Private Wealth. His responsibilities include chairing the Asset Allocation Committee and overseeing the investment administration, portfolio oversight, and fixed income and equity trading functions.

Explore companion resources designed to expand your knowledge and confidence.

Collection