Consumer and commercial banking products and services are offered through CIBC Bank USA. Member FDIC and Equal Housing Lender. All loans are subject to credit approval. Trust services and investment products are offered by CIBC Private Wealth Management. CIBC Private Wealth Management includes CIBC National Trust Company, CIBC Delaware Trust Company and CIBC Private Wealth Advisors, Inc. (a registered investment adviser) all of which are wholly owned subsidiaries of CIBC Private Wealth Group, LLC — and the private banking division of CIBC Bank USA. Trust services and investment products are not FDIC insured, not deposits or obligations of, or guaranteed by, CIBC Bank USA or CIBC National Trust Company, and are subject to investment risk, including loss of principal.

Commercial real estate products and services offered by CIBC Bank USA and CIBC Inc.

CIBC Capital Markets is a trademark brand name under which CIBC and some of its subsidiaries, including CIBC World Markets Inc., CIBC World Markets Corp. and CIBC Bank USA, provide different products and services. Capital Markets products are not FDIC insured; not deposits or obligations of, or guaranteed by, CIBC Bank USA; and are subject to investment risk, including loss of principal.

This website is not intended for use by residents of the European Union (EU).

The CIBC Logo is a registered trademark of CIBC, used under license.

©2026 CIBC Bank USA.

We provide the latest developments and potential economic impacts and implications of the evolving tariff situation

Recap

The new administration has opened the policy floodgates in the weeks following the inauguration, signing more than 70 executive orders in the first month—surpassing the combined total of signed orders by the Biden, Obama and first Trump administrations during similar time periods. During his campaign, President Donald Trump promised aggressive action on trade policy and has begun to deliver on a range of tariff proposals with implications for the global economy and markets. On February 3, Trump signed an order to impose a 25% tariff on most imports from Canada and Mexico, along with an additional 10% tariff on Chinese goods. Both Mexico and Canada negotiated 30-day delays in the start date in exchange for measures to tighten border security. What has transpired since then?

New Tariffs

Following the February announcements, President Trump proposed additional tariffs: a 25% tariff on steel and aluminum imports starting March 12 and on automobiles beginning April 2. He also signed an order to study broad reciprocal tariffs against any trading partner to counter a wide range of existing trade barriers. Currently, only the 10% tariff on Chinese imports is in effect. As of this writing, Trump has confirmed his intention to implement tariffs on Mexico and Canada starting March 4. It remains to be seen how much, if any, of the announced increases will be implemented and how trading partners will react.

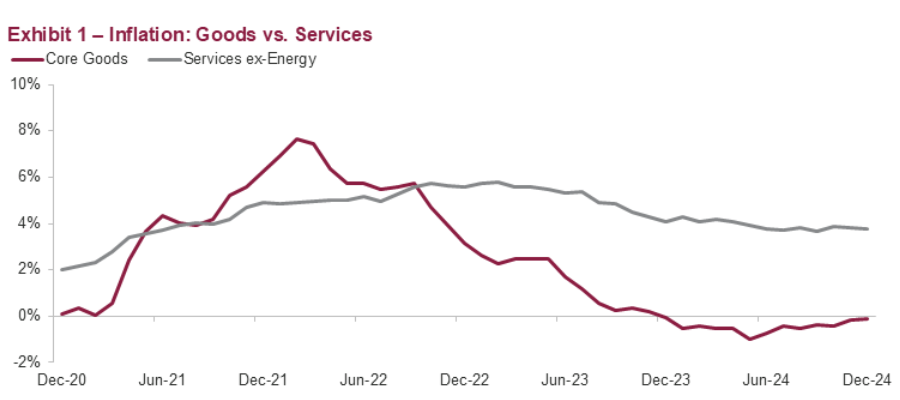

Raising tariffs can trigger various market responses, including higher prices, supply chain reconfigurations, and consumer substitution for cheaper alternatives. The first Trump administration levied a narrower set of tariffs on steel and aluminum imports, which led to increases in US prices and lower production levels in those sectors. The proposed tariffs are much broader than the actions taken in 2018 and 2019 and come at a time when improvements in inflation appear to have stalled. The trailing 12-month rate of change in prices in the Federal Reserve’s (Fed) preferred inflation gauge stood at 2.8% through the end of 2024,1 which is 0.1% higher than the low recorded in June of 2024. Prices for “core” goods (excluding food and energy categories) fell between the peak in inflation and the June low, contributing significantly to an overall improvement in US inflation.

As was the case in 2018 and 2019, tariffs resulted in a one-time increase in the price level of affected goods, leading to an immediate increase in the annual rate of inflation. However, in the second year, the annual rate of change flattened out, all else being equal. During late 2018 and 2019, the Fed opted to “look through” these temporary price hikes and instead focused on lowering interest rates to offset the drop in economic activity.

Government jobs, labor markets and the US consumer Trump’s team is exploring funding options for expiring income tax cuts, but tariffs are unlikely to cover the full amount of revenue loss projected by the Congressional Budget Office. The Department of Government Efficiency (DOGE) has been deployed to several agencies to root out fraud and what the administration deems to be unnecessary spending. Early estimates of job cuts associated with DOGE’s actions and a federal government buyout offer are wide-ranging, and it will take several months to see the full impact in economic statistics.

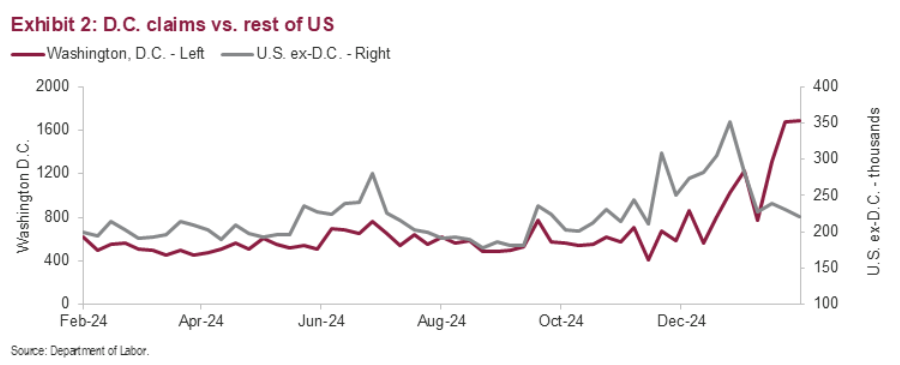

We will monitor weekly releases of claims for unemployment insurance to assess the effect on labor markets. So far, there has been a small increase in jobless claims focused in the Washington D.C. area. We expect the cuts to broaden into Virginia, Maryland, and beyond, leading to a decline in total federal government payrolls in the coming months. Much of the recent strength in the US economy is based on consumer spending, which is a function of job growth. Federal employment represents less than 1.6% of total non-farm payrolls, and we expect the overall impact to consumer spending to be restrained due to strength in the private sector and a relatively high level of job openings outside the government sector.

Implications

Policy changes on multiple fronts—trade, spending, international diplomacy, and others—create significant fissures in the old order, leading to greater uncertainty and potential for higher volatility. However, as we head into this period of change, the US economy is strongly positioned, with projections indicating slightly slower growth but continued robust earnings growth across various sectors. Continuous monitoring of trade negotiations, labor market trends, and pricing in core goods sectors will be essential to assess any emerging challenges.

We will continue to monitor and keep investors apprised of the evolving tariff situation. If you have any questions, please do not hesitate to contact a member of your CIBC Private Wealth team.

Gary Pzegeo, CFA,is co-chief investment officer of CIBC Private Wealth. His responsibilities include chairing the Asset Allocation Committee and overseeing the investment administration, portfolio oversight, and fixed income and equity trading functions.

Explore companion resources designed to expand your knowledge and confidence.

Collection