Related solution

Investment management

Turning our investment legacy into

long-term growth for your portfolio.

Consumer and commercial banking products and services are offered through CIBC Bank USA. Member FDIC and Equal Housing Lender. All loans are subject to credit approval. Trust services and investment products are offered by CIBC Private Wealth Management. CIBC Private Wealth Management includes CIBC National Trust Company, CIBC Delaware Trust Company and CIBC Private Wealth Advisors, Inc. (a registered investment adviser) all of which are wholly owned subsidiaries of CIBC Private Wealth Group, LLC — and the private banking division of CIBC Bank USA. Trust services and investment products are not FDIC insured, not deposits or obligations of, or guaranteed by, CIBC Bank USA or CIBC National Trust Company, and are subject to investment risk, including loss of principal.

Commercial real estate products and services offered by CIBC Bank USA and CIBC Inc.

CIBC Capital Markets is a trademark brand name under which CIBC and some of its subsidiaries, including CIBC World Markets Inc., CIBC World Markets Corp. and CIBC Bank USA, provide different products and services. Capital Markets products are not FDIC insured; not deposits or obligations of, or guaranteed by, CIBC Bank USA; and are subject to investment risk, including loss of principal.

This website is not intended for use by residents of the European Union (EU).

The CIBC Logo is a registered trademark of CIBC, used under license.

©2026 CIBC Bank USA.

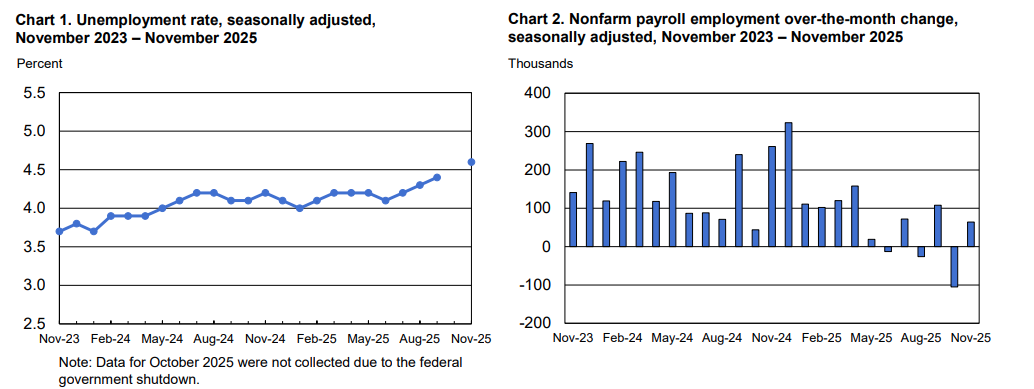

A summary of the U.S. Bureau of Labor Statistics November 2025 Employment Report

The U.S. economy added 64,000 jobs in November and lost 105,000 jobs in October according to the Bureau of Labor Statistics (BLS) survey of employers. Today’s employment data is unusual in several respects due to the Government shutdown. First, the BLS released two months of payroll data based on their survey of businesses, but only one unemployment rate based on an abbreviated October survey of individuals. Secondly, the shutdown and previously announced layoffs in the Government sector drove a 157,000 reduction in payrolls in October. The November increase was above expectations for a gain of 50,000. Payrolls for August and September were revised lower by 33,000. Overall, employment growth remains very slow. The economy has added 22,300 jobs on average over the trailing 3 months versus a 209,300 average at the end of 2024. Away from the Government sector, private sector job growth is also slower than average and very narrow. Private payrolls have increased by an average 75,000 jobs over the last three months with Health Care & Social Assistance jobs representing over 83% of that increase. The three-month average private sector gain is over 100,000 below the pace generated at the end of 2024.

The BLS’s survey of households reported an increase in the unemployment rate to 4.6% in November from 4.4% in September. The size of the U.S. labor force expanded by 323,000 with new entrants to the labor force representing over 90% of the change. The survey of households revealed an increase in the number of unemployed individuals by 228,000 since September with layoffs of temporary positions up by 171,000.

Average hourly earnings – a proxy for wage growth – rose 0.1% in November and 0.4% in October. The trailing 12-month increase was 3.5% vs. a 4.0% run rate at the end of 2024. November earnings data was below consensus expectations of a 0.3% increase.

Bottom line: Re-opening of the Government is helping to lift the economic fog for the Fed and markets at the margin despite a few remaining distortions. Employment growth remains slow, but is not as bad as suggested by the headlines once you strip out the adjustments to the Government sector. Wage growth is decelerating at a slow pace. Taken together, the Fed may be inclined to continue easing in 2026 but will likely want to see a “clean” report on December jobs. Market implied odds of a cut at the Fed’s January 28th meeting were at 25% following today’s release, approximately unchanged since the Fed’s last meeting on December 10.