Related solution

Investment management

Turning our investment legacy into

long-term growth for your portfolio.

Consumer and commercial banking products and services are offered through CIBC Bank USA. Member FDIC and Equal Housing Lender. All loans are subject to credit approval. Trust services and investment products are offered by CIBC Private Wealth Management. CIBC Private Wealth Management includes CIBC National Trust Company, CIBC Delaware Trust Company and CIBC Private Wealth Advisors, Inc. (a registered investment adviser) all of which are wholly owned subsidiaries of CIBC Private Wealth Group, LLC — and the private banking division of CIBC Bank USA. Trust services and investment products are not FDIC insured, not deposits or obligations of, or guaranteed by, CIBC Bank USA or CIBC National Trust Company, and are subject to investment risk, including loss of principal.

Commercial real estate products and services offered by CIBC Bank USA and CIBC Inc.

CIBC Capital Markets is a trademark brand name under which CIBC and some of its subsidiaries, including CIBC World Markets Inc., CIBC World Markets Corp. and CIBC Bank USA, provide different products and services. Capital Markets products are not FDIC insured; not deposits or obligations of, or guaranteed by, CIBC Bank USA; and are subject to investment risk, including loss of principal.

This website is not intended for use by residents of the European Union (EU).

The CIBC Logo is a registered trademark of CIBC, used under license.

©2026 CIBC Bank USA.

After more than a decade of U.S. equity market dominance, the case for a structurally diversified equity portfolio with international exposure is more compelling than ever. While the U.S. market accounts for a significant share of global market capitalization, it does not capture the full scope of global growth and innovation. International equities provide access to a wider range of economic cycles, sectors, currencies, and policy regimes. This diversity creates valuable opportunities for active managers to identify attractive investments and dynamically adjust allocations as market conditions evolve. Historically, periods of U.S. and international outperformance have tended to alternate. By combining both, investors can tap into a broader and more resilient set of return drivers.

Exhibit 1: U.S. and international equity returns fluctuate over time

S&P 500 Index vs. MSCI ACWI ex U.S. Index Returns

Diversification and valuation

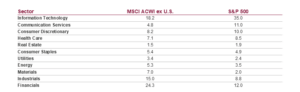

International equities offer meaningful diversification benefits. Non-U.S. markets generally are less concentrated in mega-cap technology companies and provide more exposure to financials, industrials, manufacturing, and energy. This sector diversity complements U.S. equity exposure, rather than competing with it. As of April 30, approximately 40% of the S&P 500 Index was concentrated in its top 10 holdings, compared with just 14% for the MSCI ACWI ex U.S. Index. The continued outperformance of the so-called “Magnificent Seven” has further increased this concentration in U.S. markets.

International markets also participate in technology-driven growth, but in different ways. The top four holdings in the MSCI ACWI ex U.S. Index—Taiwan Semiconductor Manufacturing, Samsung Electronics, ASML Holding, and SK Hynix—are global technology leaders. By excluding high-quality companies simply because they are headquartered outside the United States, investors risk missing important drivers of global innovation while remaining concentrated in a narrow group of U.S. technology names. While artificial intelligence is transformative, leadership cycles have historically rotated. Market regimes do not last forever.

Different monetary and fiscal cycles across regions can also enhance diversification, as economies respond to their own conditions. Increasingly, international markets are placing greater emphasis on shareholder returns, which may support stronger corporate governance and investment prospects. Reshoring and global supply chain restructuring could also create new regional winners. Currency exposure adds another dimension to diversification. While currency fluctuations can help or hinder returns in the short term, foreign currency exposure can diversify dollar-centric risk over the long run. Investors can choose between hedged and unhedged strategies based on their risk tolerance and outlook.

For the trailing one- and three-year periods ended April 30, 2026, currency contributed 22% of relative performance between the MSCI ACWI ex U.S. Index and the S&P 500 Index over the past year. Even though the MSCI ACWI ex U.S. Index underperformed the S&P 500 Index over the trailing three-year period, currency exposure still made a small positive contribution. Investors have the flexibility to choose hedged or unhedged strategies based on their preferences and risk tolerance.

Exhibit 2: MSCI ACWI ex U.S. and S&P 500 Index Sector Weights

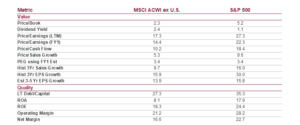

International markets continue to offer more attractive valuations than the United States. Historically, starting valuations have played a crucial role in determining long-term returns. International markets trade at discounts on price-to-earnings and price-to-book ratios, while also providing higher dividend yields and appealing quality metrics. Some U.S. valuation premium is justified by stronger profitability, innovation, and corporate governance. However, the current valuation gap may overstate these advantages.

Exhibit 3: Valuation, growth and quality metrics

Positioning for the future

As with any investment, international investing involves risk. Geopolitical uncertainty and slower structural growth in some regions remain key considerations, and U.S. exceptionalism may persist. However, the benefits of international diversification do not rely on international markets outperforming the U.S. every year.

After an extended period of U.S. equity dominance, now is an opportune time for investors to reassess whether their current allocations are truly positioned for resilience and long-term success. Increasing international exposure is not about chasing returns—it is about broadening the investment universe, reducing concentration risk, and tapping into the full spectrum of global innovation and growth. While the U.S. market will likely remain a key driver of global returns, relying solely on U.S. equities may leave portfolios vulnerable to shifts in market leadership and sector dynamics.

By incorporating international equities, investors can access world-class companies, benefit from diverse economic cycles and policy environments, and enhance the potential for more balanced, risk-adjusted returns. In today’s interconnected and rapidly evolving markets, a globally diversified approach is not just prudent—it is essential for those seeking to build robust portfolios and capture opportunities wherever they arise.