Related solution

Investment management

Turning our investment legacy into

long-term growth for your portfolio.

Consumer and commercial banking products and services are offered through CIBC Bank USA. Member FDIC and Equal Housing Lender. All loans are subject to credit approval. Trust services and investment products are offered by CIBC Private Wealth Management. CIBC Private Wealth Management includes CIBC National Trust Company, CIBC Delaware Trust Company and CIBC Private Wealth Advisors, Inc. (a registered investment adviser) all of which are wholly owned subsidiaries of CIBC Private Wealth Group, LLC — and the private banking division of CIBC Bank USA. Trust services and investment products are not FDIC insured, not deposits or obligations of, or guaranteed by, CIBC Bank USA or CIBC National Trust Company, and are subject to investment risk, including loss of principal.

Commercial real estate products and services offered by CIBC Bank USA and CIBC Inc.

CIBC Capital Markets is a trademark brand name under which CIBC and some of its subsidiaries, including CIBC World Markets Inc., CIBC World Markets Corp. and CIBC Bank USA, provide different products and services. Capital Markets products are not FDIC insured; not deposits or obligations of, or guaranteed by, CIBC Bank USA; and are subject to investment risk, including loss of principal.

This website is not intended for use by residents of the European Union (EU).

The CIBC Logo is a registered trademark of CIBC, used under license.

©2026 CIBC Bank USA.

Extended standoff in the Strait of Hormuz as energy demand rises seasonally

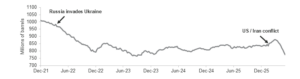

Inventory drawdowns act as a price buffer… but for how long?

Crude oil inventory levels, including Strategic Petroleum Reserve

Source: Bloomberg, Energy Information Administration, as of June 10, 2026.

Oil prices have increased from $67/barrel right before the US/Iran conflict broke out to $85/barrel at the end of last week* (with a brief trip over $100/barrel in May). While significant, this rise has been milder than many forecasts, and the US economy has so far weathered the storm.

The supply shock from the obstruction of the Strait of Hormuz has largely been absorbed by drawing down oil inventories. The chart illustrates that crude stocks have declined since the conflict began. If the Strait obstruction drags on while seasonal demand for energy rises, inventories may soon offer less protection against further price increases. A durable ceasefire and opening of the Strait would ease pressure on energy prices, though restoring Middle East production to pre-conflict levels could take several months.

The US inventory drawdown is mostly due to releases from the government’s Strategic Petroleum Reserve (SPR). However, SPR flows are limited by the substantial depletion in 2022, which was used to curb price spikes following Russia’s invasion of Ukraine. Neither the previous nor current administration materially replenished the SPR, leaving less policy flexibility today.

What we’re watching this week:

Wednesday: New Federal Reserve Chair Kevin Warsh will lead his first monetary policy meeting. The FOMC is widely expected to leave interest rates unchanged. Markets will focus on whether guidance shifts from a lower rate bias in the future to a more neutral stance. May Retail Sales will be released. Despite poor sentiment and affordability pressures, consumer spending has been resilient in recent months.

Throughout the week: Central banks in Japan, the UK, and Switzerland will announce policy decisions. A key question will be whether they follow the ECB’s lead and raise rates.

Friday: US stock and bond markets are closed for the Juneteenth holiday.