Related solution

Investment management

Turning our investment legacy into

long-term growth for your portfolio.

Consumer and commercial banking products and services are offered through CIBC Bank USA. Member FDIC and Equal Housing Lender. All loans are subject to credit approval. Trust services and investment products are offered by CIBC Private Wealth Management. CIBC Private Wealth Management includes CIBC National Trust Company, CIBC Delaware Trust Company and CIBC Private Wealth Advisors, Inc. (a registered investment adviser) all of which are wholly owned subsidiaries of CIBC Private Wealth Group, LLC — and the private banking division of CIBC Bank USA. Trust services and investment products are not FDIC insured, not deposits or obligations of, or guaranteed by, CIBC Bank USA or CIBC National Trust Company, and are subject to investment risk, including loss of principal.

Commercial real estate products and services offered by CIBC Bank USA and CIBC Inc.

CIBC Capital Markets is a trademark brand name under which CIBC and some of its subsidiaries, including CIBC World Markets Inc., CIBC World Markets Corp. and CIBC Bank USA, provide different products and services. Capital Markets products are not FDIC insured; not deposits or obligations of, or guaranteed by, CIBC Bank USA; and are subject to investment risk, including loss of principal.

This website is not intended for use by residents of the European Union (EU).

The CIBC Logo is a registered trademark of CIBC, used under license.

©2026 CIBC Bank USA.

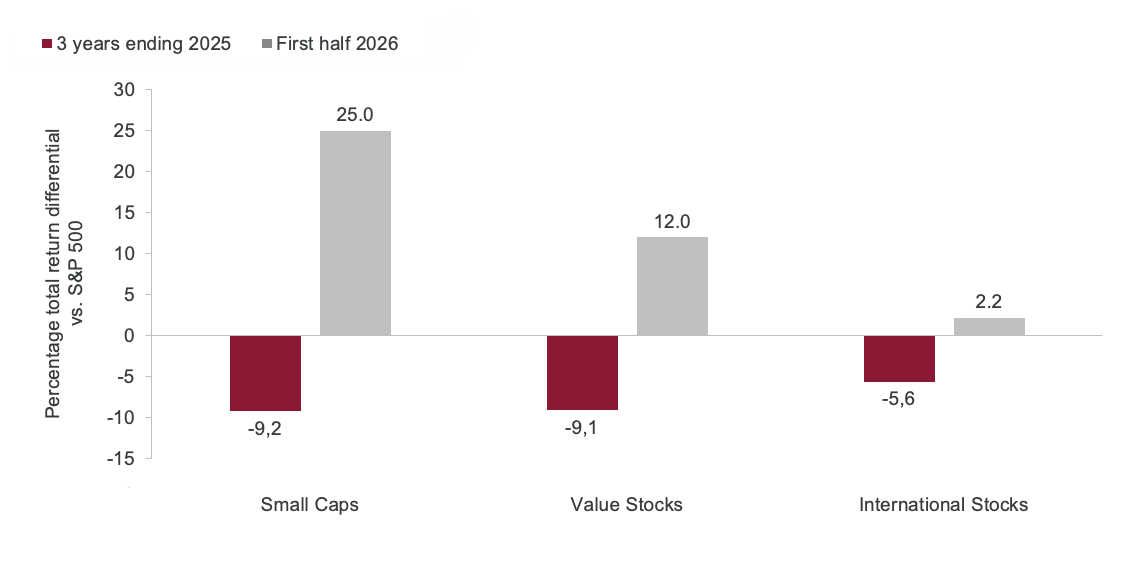

Leaders from the last three years have lagged so far in 2026

Relative performance vs. the S&P 500, annualized

Source: Bloomberg, as of June 30, 2026. Annualized total returns. Indices used are Russell 2000, Russell 1000 Value, and MSCI All Country World ex-US Index.

Financial markets had plenty to contend with in the first half of 2026: the US/Iran conflict, higher inflation readings, and diminished expectations for interest rate cuts from the Federal Reserve. Nevertheless, the S&P 500 posted a solid total return of 10.2% for the six-month period.

The bull market that began in late 2022 continues. However, the drivers pushing equity benchmarks higher in the first half of the year marked a reversal from what dominated performance in the 2023-2025 period. That three-year timeframe was dominated by the Magnificent Seven mega-cap stocks and others considered beneficiaries of the artificial intelligence boom. An index of the Magnificent Seven stocks rose at a 63% annualized rate over that time period but was actually down slightly in the first half of 2026.

The chart above illustrates other trend reversals evident this year. Small companies, value stocks and international equities have all outperformed in 2026 after significantly lagging the S&P 500 over the prior three calendar years. While underperformance by prior market leaders can be unnerving to investors, rotation toward a broader set of opportunities usually helps to extend equity bull markets

Monday: The ISM Services Index for June is released. Private service-producing industries account for over 70% of total US economic output.

Wednesday: Minutes from the FOMC’s mid-June meeting will be available. Investors are interested in the deliberations that occurred during Chair Warsh’s first meeting as leader.